In the complex world of corporate finance, some tools reveal more than just numbers. The balance sheet shows assets, and the income statement reflects profitability. But the cash flow statement? It goes one step further.

It unveils actual cash flows, providing insight into a company's true financial health. After all, what good are assets and earnings if your cash isn’t flowing?

Before you start, you can refresh your knowledge with our cash management article.

What you’ll learn in this article

- The purpose of the cash flow statement

- Its key components

- How entrepreneurs can use the cash flow statement to assess financial health

- The key metrics you should know in relation to the cash flow statement

TL;DR

- Real-time insight into liquidity: the cash flow statement tracks all cash inflows and outflows across operations, investments, and financing. It highlights how much actual cash a business generates and uses, unlike the income statement, which relies on accounting figures.

- Strategic and operational control tool: it supports liquidity planning, investment decisions, stakeholder transparency, and early detection of financial risks. Operating cash flow is especially crucial as a sign of sustainable business performance.

- Monitoring and optimization made easy: with software tools can create real-time, customizable cash flow statements by team, category, or project, enabling better decision-making, efficient working capital use, and internal financing of growth.

Definition: What is the cash flow statement?

The cash flow statement provides a detailed overview of all cash inflows and outflows of a company within a specific period.

It helps determine your cash position. Unlike the income statement, which focuses on accounting-based revenues and expenses, the cash flow statement highlights actual cash movements.

This focus on real cash flows shows how well a company can generate liquidity. Insights from the cash flow statement are crucial for financial planning and identifying potential shortfalls.

Understanding cash flow statements

While the income statement tells you about profits and the balance sheet shows assets and liabilities, the cash flow statement reveals what truly matters in day-to-day business: how much money is actually moving in and out of the company.

It’s structured into three parts:

- Operating activities shows how much cash your business generates from its core activities, selling products or services.

- Investing activities reflects how you use money for the future, for example buying machines, software, or other assets.

- Financing activities captures the movement of capital: loans, repayments, or dividends.

Together, these three sections show whether your business can fund itself, grow sustainably, and handle short-term obligations.

This is the real power of the cash flow statement

But the real power of the cash flow statement lies in what it reveals beyond the numbers: stability, resilience, and the timing of payments.

A company might be profitable on paper but still struggle with liquidity. The cash flow statement exposes these gaps. It helps companies make better decisions, monitor their financial health, and avoid surprises: whether it’s a looming cash crunch or the right time to invest.

In short, the cash flow statement is the financial reality check every business needs.

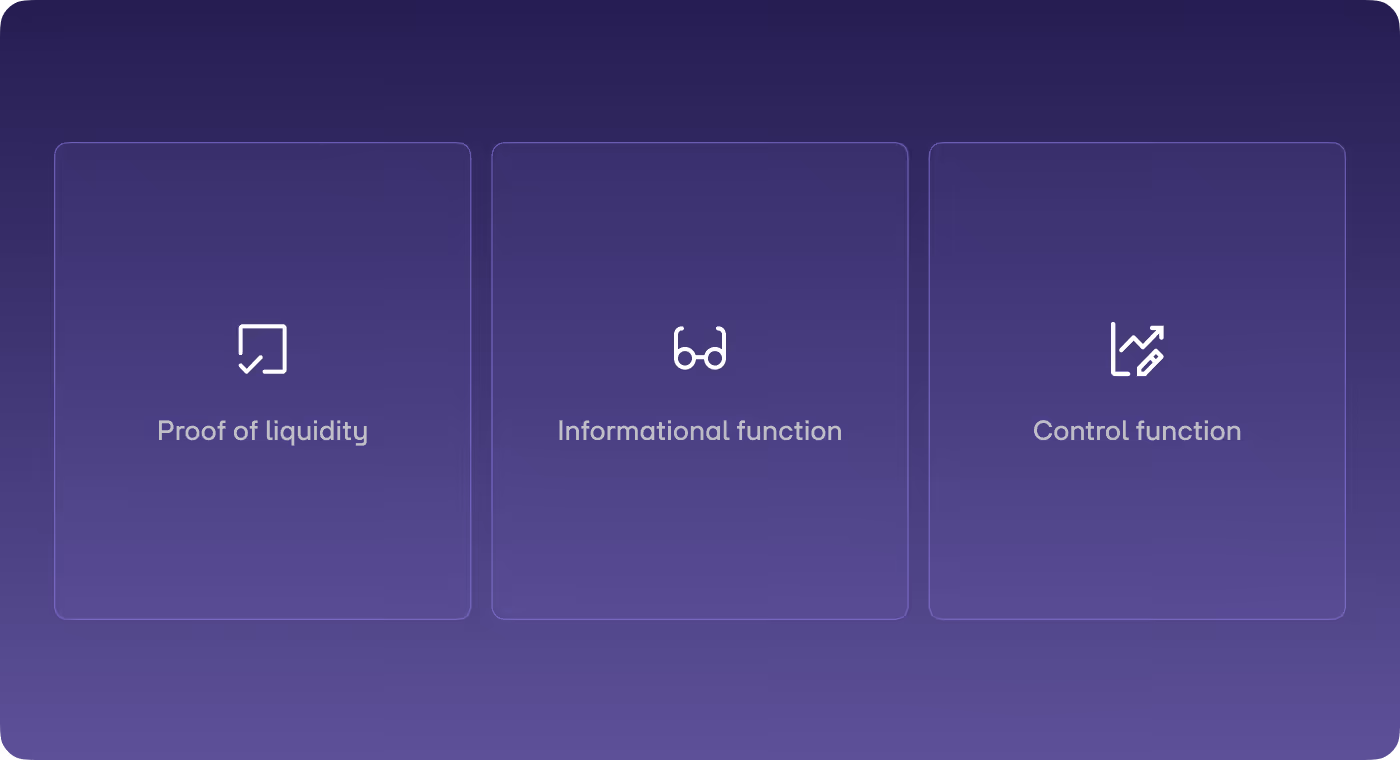

What does a cash flow statement help with?

The cash flow statement plays a vital role in financial analysis and cash flow planning. It serves several important functions, including:

Liquidity proof

- Documentation of solvency

- Evidence of cash inflows and outflows

- Basis for liquidity planning

Information function

- Transparency for stakeholders

- Basis for investment decisions

- Evaluation tool for lenders

Control function

- Monitoring financial flows

- Early detection of liquidity bottlenecks

- Efficiency control of working capital

Master your cash flow

We help you get a clear and detailed view of your cash flow statement – based on real-time data.

Start 14-day free trialComponents of a cash flow statement

The cash flow statement consists of three main sections:

- Operating activities

- Investing activities

- Financing activities

1. Operating activities: a closer look at core business

- Includes all cash flows from regular business operations

- Shows the company’s ability to generate liquidity from core activities

- Considered the most important indicator of sustainable business performance

Operating cash flow examines inflows and outflows from day-to-day business operations.

Cash inflows from operations

- Customer payments

- Interest received

- Other operating cash inflows

Cash outflows from operations

- Payments to suppliers

- Payroll expenses

- Interest payments

- Tax payments

Example calculation: operating cash flow

Factors influencing operating activities

Various factors impact operating cash flow, such as managing receivables, payables, and inventory. An optimized receivables management strategy, like shortening payment terms or implementing a just-in-time (JIT) system, can significantly improve liquidity.

Receivables

- Average days sales outstanding (DSO)

- Measures to shorten the cash conversion cycle

- Impact of different payment terms

Payables

- Optimization of payment terms

- Early payment discounts vs. extended payment terms

- Supplier financing options

Inventory

- Just-in-time vs. safety stock

- ABC analysis for inventory optimization

- Seasonal stockpiling

Example: optimizing working capital for operating cash flow

Initial situation of a mid-sized manufacturing company:

Optimization measures

- Implementing factoring for 50% of receivables

- Introducing a JIT system

- Renegotiating supplier terms

Results after optimization

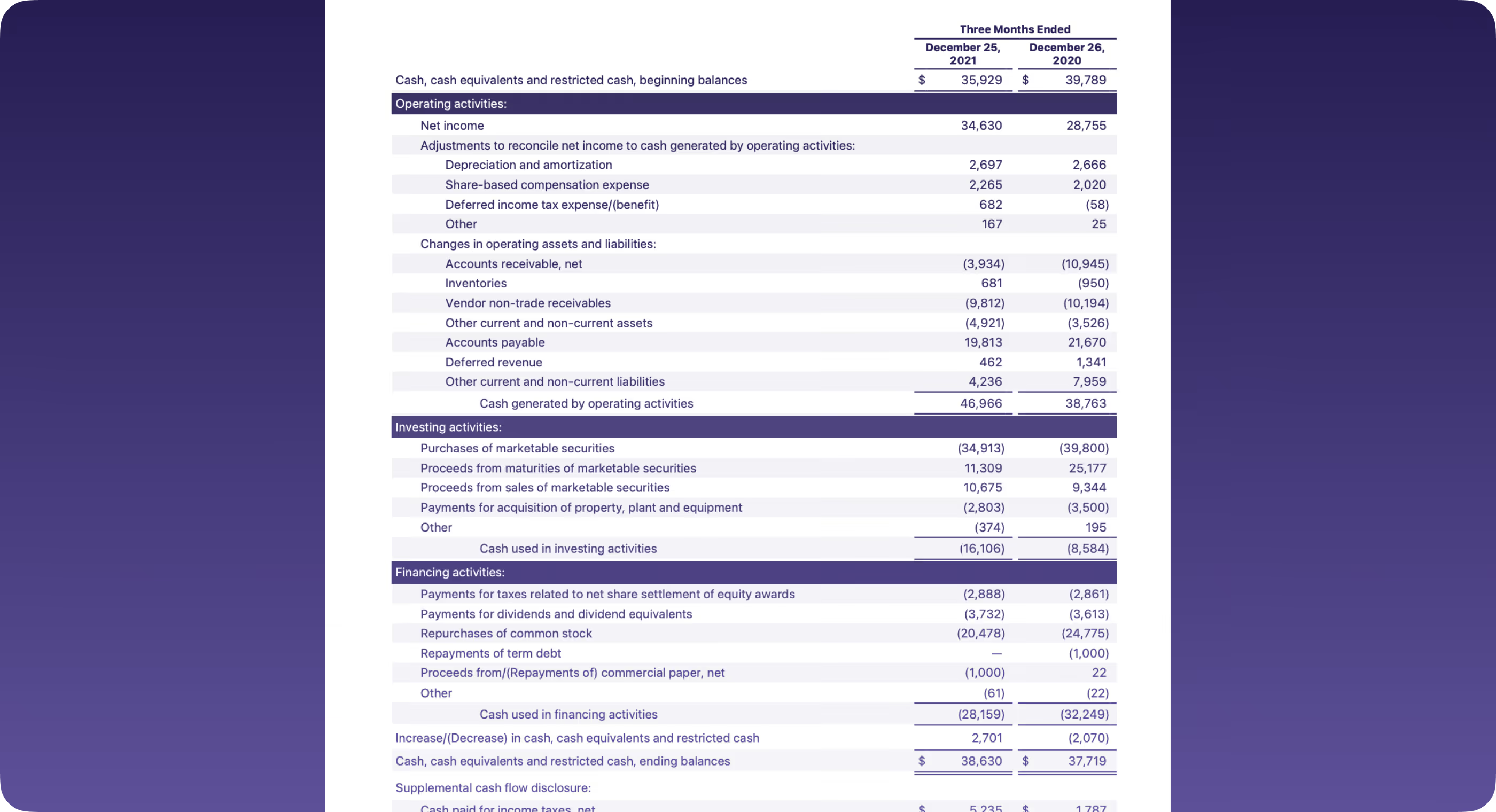

Example of a cash flow statement

2. Investing activities: securing the future

The investing activities represent investments, include purchases and sales of fixed assets, and reflect the company’s long-term growth strategy.

It racks cash inflows and outflows related to investment activities and provides insights into a company's long-term strategic direction.

Cash inflows from investing activities

- Sale of fixed assets

- Divestment of equity stakes

- Sale of securities

Cash outflows from investing activities

- Purchase of fixed assets

- Acquisition of equity stakes

- Investment in intangible assets

Example calculation: investing activities

3. Financing activities: capital structure and payouts

The financing activities document capital movements with equity and debt investors, include dividend payments and loan borrowings/repayments, and reflect the company’s financing strategy. Financing cash flow shows how a company raises and uses capital: whether for growth or shareholder payouts. They reveal the company’s financing strategy and offers insight into stability and future plans.

Cash inflows from financing activities

- Capital increases

- Loan borrowings

- Issuance of bonds

Cash outflows from financing activities

- Dividend payments

- Loan repayments

- Share buybacks

A positive financing cash flow signals incoming capital for expansion or strategic investments. A negative figure can indicate debt reduction or shareholder distributions. The key is context: Is it sustainable growth or risky financing?

Analysis of the cash flow statement

Theory is great, but how do specific business decisions impact the cash flow statement? Every company needs to make its money work. When investing, it’s crucial to know which decisions will pay off in the long run. Let’s look at two concrete examples, investing cash flow and operating cash flow.

Investment decision: impact on investing activities

A company spends €1 million on a new machine. The machine generates €250,000 in annual cash flow and retains a residual value of €100,000 after five years. Is the purchase worth it? The ROI provides the answer.

ROI calculation

Impact on the cash flow statement

A 35% ROI is solid. The investment pays off.

The machine purchase immediately impacts investing cash flow as a significant outflow in the year of acquisition. In the following years, operating cash flow improves because the machine generates €250,000 annually.

At the end of its lifespan, the €100,000 residual value flows back.

The large initial cash outflow is offset by stable yearly inflows and the final resale value. The investment temporarily burdens investing cash flow but strengthens operating cash flow in the long run.

Make-or-buy decision: impact on operating activities

One of the most strategic decisions a company faces: produce in-house or outsource? The answer lies in the numbers and affects operating cash flow.

In-house production

- Investment: €500,000

- Annual fixed costs: €100,000

- Variable cost per unit: €50

Outsourcing

- Price per unit: €80

- No fixed costs

The key question: Where is the break-even point?

Break-even calculation

Analysis and impact on the cash flow statement

Producing more than 3,333 units makes in-house production more cost-effective. Below that, outsourcing is the smarter choice. In-house production requires more upfront capital (reducing investing cash flow) but improves operating cash flow if production volume is high. Outsourcing conserves liquidity but puts more strain on operating cash flow per unit produced.

Cash flow statement: the bottom line

Not only the amount of cash flow matters but also its structure and stability. Three key questions help you analyze the cash flow statement:

- How stable is cash flow over time? Fluctuations can pose a risk.

- What percentage of total cash flow comes from operating cash flow? A high percentage indicates a solid business model.

- How sustainable are the earnings? One-time special effects can distort the picture.

In qualitative cash flow analysis, you differentiate between sustainability indicators (ratio of operating to total cash flow, stability of cash flows over time, and quality of earnings) and growth indicators (investment ratio, self-financing ratio, payout ratio).

These factors determine how well a company withstands crises and whether it can grow on its own. They are essential for analyzing the cash flow statement.

Those who understand their cash flow statement can manage it and avoid bottlenecks. Entrepreneurs should regularly compare actual cash flow with planned figures, check outstanding receivables and liabilities, and monitor inventory levels.

Regular cash flow monitoring and an early warning system are crucial. Metrics such as liquidity ratio or working capital ratio help identify potential financial bottlenecks early and take corrective action.

Establishing cash flow monitoring and an early warning system

Cash flow reveals whether a company is financially healthy. But it doesn’t run itself. Structured monitoring helps minimize liquidity risks:

Cash flow monitoring

- Plan vs. actual comparison: Does actual cash flow deviate from the liquidity planning?

- Receivables management: Have the most important customer payments been received?

- Check liabilities: Which invoices are about to become due?

- Analyze inventory: Is too much capital tied up in stock?

However, this analysis alone is not enough. You need an early warning system that monitors critical metrics:

Early warning system

- Liquidity ratio 1 (<0.2): Is immediately available cash sufficient to cover short-term liabilities?

- Working capital ratio (<1.2): Is current assets sufficient to meet short-term obligations?

- Operating cash flow / short-term liabilities (<0.3): Does ongoing business activity cover short-term debts?

How healthy is your company? Use benchmarks

In addition to individual analyses, benchmark values can help. You can review certain ratios for your cash flow statement analysis and use them as references:

- If operating cash flow / total cash flow is >75% the company has a solid financial foundation.

- If investment ratio is >15% the company is growth-oriented.

- If self-financing ratio is >100% the company is financially independent from external lenders.

- If payout ratio is <50% the company has a sustainable financial strategy.

How to link balance sheet, P&L, and cash flow statement

The full significance of a cash flow statement emerges only in conjunction with other financial reports: the balance sheet and the P&L.

Therefore, the cash flow statement should never be seen as single unit but should be rather analyzed in comparison to other financial reports.

Integrated analysis: the key metrics

A deeper dive reveals critical interconnections:

- Cash conversion rate = Operating cash flow / EBIT → How much profit is actually converted into cash?

- Working capital efficiency = Working capital / revenue → How efficiently is tied-up capital used?

- Investment coverage = Operating cash flow / investments → Can investments be financed internally?

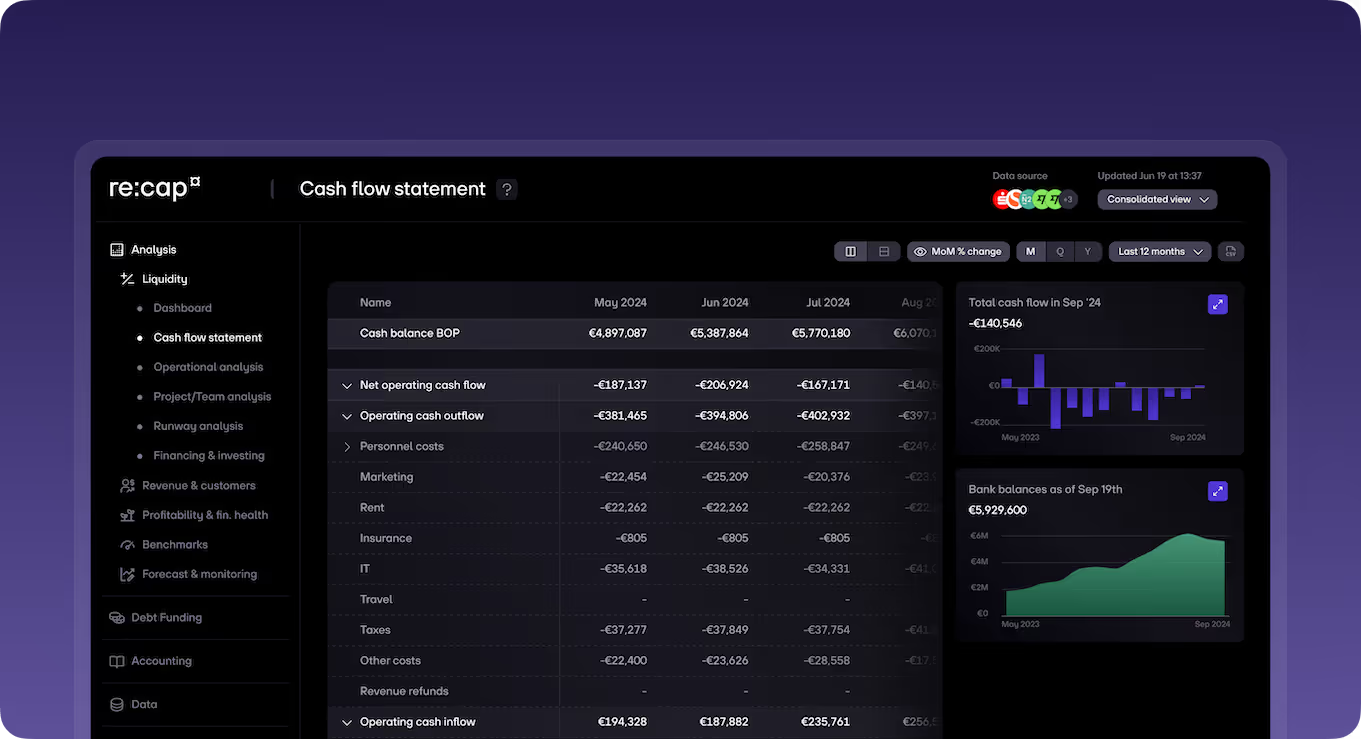

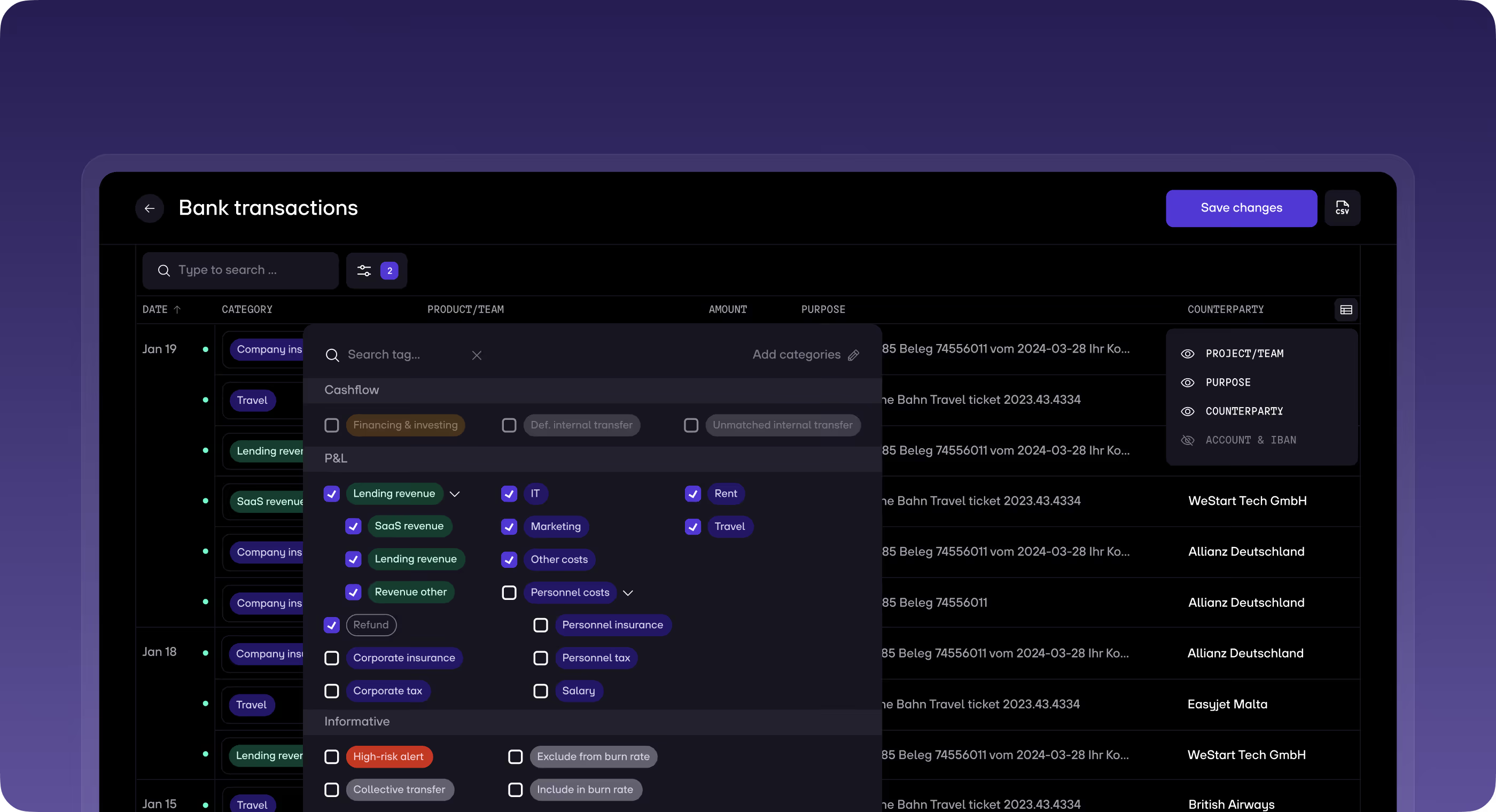

Cash flow statement at re:cap

re:cap provides businesses with cash flow software to manage and plan liquidity while offering financing when needed. A cash flow statement is part of this solution. You can access it in real-time, with live bank transaction processing, ensuring an up-to-date cash flow overview.

You can also create a cash flow statement at project and team levels by assigning transactions accordingly. This allows better cash data organization and deeper insights. It enables you to:

- Categorize your cash flow in more detail and generate a cash flow statement with only relevant transactions (e.g., IT salaries only).

- Customize transactions by team, business unit, or project to get tailored reports and understand liquidity at every level.

- Allocate expenses to different categories (COGS, operating expenses, financing costs, department, team, country, etc.).

The re:cap cash flow statement includes the following categories:

- Cash balance: the total cash balance at the beginning (BOP) and end of a period (EOP).

- Net cash flow: the total cash flow for the period, including optional breakdowns of inflows and outflows.

- Net operating cash flow: the total cash flow from all operating activities, showing how much cash the company generates from its products or services. Optional breakdowns into inflows, outflows, and detailed categories.

- Net cash flow from financing and investments: the total cash flow from all financing and investment activities, showing how cash is used for non-operating activities like debt or equity transactions. Optional breakdowns into inflows and outflows.

- Net intracompany cash flow: the total cash flow between company accounts or between subsidiaries' accounts. Optional breakdowns into inflows and outflows.

If you're looking for cash management software, we compare different providers like:

Summary: Cash flow statement

Forget what the income statement or balance sheet might suggest. If you really want to know how a business is doing, follow the money.

That’s what the cash flow statement does. It shows what matters most in everyday business: how much cash actually comes in, and how much goes out.

Together, these numbers tell a simple but crucial story: Can the business sustain itself, grow responsibly, and cover its short-term obligations?

But the true value of the cash flow statement lies beneath the surface. It reveals what balance sheets often hide: timing gaps, liquidity risks, and early warning signs.

A company might be profitable on paper but broke in practice. Cash flow doesn’t lie. It forces a reality check.

Q&A: Cash flow statement

What are the 3 types of cash flow statement?

The cash flow statement is divided into three sections:

- Operating activities: cash from core business operations (e.g., sales, payments to suppliers).

- Investing activities: cash related to buying or selling assets (e.g., equipment, securities).

- Financing activities: cash from borrowing or repaying debt, issuing shares, or paying dividends.

What are the 5 items on a cash flow statement?

The key items typically include:

- Net cash from operating activities

- Net cash from investing activities

- Net cash from financing activities

- Net increase or decrease in cash

- Cash at the beginning and end of the period

How to calculate a cash flow statement?

Use either:

- The direct method, listing all cash inflows and outflows directly.

- The indirect method, starting with net income and adjusting for non-cash items and changes in working capital.

Both lead to the same result: total cash flow over the period.

What is the difference between the income statement and the cash flow statement?

The income statement shows profitability based on accrual accounting (including non-cash items like depreciation). The cash flow statement shows actual cash movement in and out of the business. Profit ≠ cash which means you can be profitable on paper but still run out of cash.

Why is profit more important than cash flow?

It isn’t always. Profit is key for long-term sustainability, but cash flow keeps the business alive day to day. Without cash, you can’t pay suppliers or employees, even if you’re profitable on paper.

What is the difference between a balance sheet and a cash flow statement?

The balance sheet is a snapshot of a company’s financial position at a specific time (assets, liabilities, equity). The cash flow statement shows how cash moved during a period. The balance sheet shows what you have; the cash flow statement shows how money moved.

Master your cash flow

We help you get a clear and detailed view of your cash flow statement – based on real-time data.

Start 14-day free trial.png)