Yes, it's a no-brainer: companies require enough capital to cover their expenses and sustain their operations.

There isn't a one-size-fits-all ideal cash balance; it varies depending on various factors and is closely tied to a company's funding.

Still, this topic is crucial. And in this article, we'll explore how to achieve the optimal cash balance using two different examples, all while leveraging re:cap's flexible financing solution.

What you'll learn in this article

- What the cash balance is

- How to read the cash balance

- How re:cap helps companies with their cash balance

TL;DR

- Your cash balance is the amount of liquid funds available to cover daily operations, investments, and unexpected expenses. It’s a key indicator of financial health. A cash balance too little puts your business at risk, too much ties up capital inefficiently.

- An ideal cash balance depends on your burn rate, fixed costs, and capital needs over time. Smart planning involves forecasting when funds are needed and aligning financing accordingly to avoid peaks and troughs.

- re:cap provides flexible, needs-based debt financing. This helps companies maintain their target cash balance without overfunding or draining resources.

Definition: What is cash balance?

Cash balance refers to the amount of cash available to a company, including short-term bank balances and deposits.

An optimized cash balance is crucial for the operational continuity of a business, covering expenses such as salaries, rent, or payments to service providers.

How to read the cash balance

The cash balance may seem like a simple number on your balance sheet, but it reveals a lot about your company’s financial health.

Reading it is about knowing how much money you have in the bank and understanding what that number means in the broader context of your company, your risks, and your growth plans.

Start with the basics: what are you looking at?

Your cash balance is listed under current assets on the balance sheet. It includes all cash and cash equivalents:

- Money in the bank

- Petty cash

- Liquid assets that can be converted to cash in less than three months.

This is your most flexible financial resource, and the one you'll rely on to cover day-to-day operations. But don’t just look at the number in isolation. The key is context.

Compare it to burn rate

To make your cash balance meaningful, compare it to your monthly burn rate: how much cash your company spends on average each month.

For example, if you burn €200K a month and your cash balance is €800K, you’ve got four months of cash runway.

That’s helpful, but not always enough, especially if your revenue is unpredictable or your costs are rising.

Runway formula

Founders and CFOs should regularly calculate months of runway:

Runway = Cash Balance / Monthly Net Burn Rate

This tells you how long you can operate without new income or funding. It’s a critical KPI in board meetings, investor pitches, and financial planning.

Analyze cash Trends, not just snapshots

The cash balance is a snapshot at a point in time but what matters most is the trend over time.

Is your cash balance steadily decreasing month-over-month? Spiking and dipping erratically? Or growing steadily as your business scales?

Use a rolling 13-week cash flow forecast to track inflows and outflows. This gives you visibility into short-term liquidity risks, helps you better plan liquidity, and to anticipate when you’ll need to raise funds, delay expenses, or reallocate capital.

Contextualize it against liabilities

A healthy cash balance also depends on your liabilities. Compare your cash balance to your short-term debts and obligations. If your liabilities exceed your cash reserves by a wide margin, that could be a red flag, even if your absolute cash balance looks high.

A €1M cash balance isn’t comforting if you owe €1.5M next quarter.

Segment operational vs. strategic cash

Another advanced move: split your cash balance into operational and strategic cash.

Operational cash is what you need to run the business: payroll, rent, software subscriptions.

Whereas strategic cash is what you might deploy for growth:

- Hiring

- Expansion

- Marketing pushes

- M&A

Keeping this mental (or spreadsheet) distinction helps you avoid tapping into critical reserves when planning for scale.

Don’t forget seasonality and timing

Cash balances can fluctuate due to seasonal revenue cycles, one-time expenses, or payment timing.

A healthy balance in January could mask an incoming dip in March if most of your customer payments hit in Q1.

Make sure your reading of the cash balance accounts for timing mismatches between revenue and costs.

Goals of cash balance

Cash balance is a critical factor in the financial planning of companies. Typically, firms require sufficient capital for three key areas:

- Covering operational costs

- Financing investments

- Hedging against uncertainties

Maintaining an adequate cash balance ensures that companies remain agile and that revenues and expenses are in a healthy balance. The definition of a "good" cash balance varies depending on the company's stage, business plan, and capital structure.

Costs of cash balance

However, having too much cash at hand also has its downsides. For instance, if companies raise too much money in a financing round, capital costs increase. Capital costs are typically higher for equity financing compared to debt financing.

While having a surplus of funds provides security, ideally, companies should deploy capital immediately.

To achieve this, they need a well-defined business plan and cash flow forecasting to determine their capital needs over time.

Approaches to cash balance

Every company has individual capital needs. Some companies are risk-averse. They prefer to maintain higher cash reserves for added security. In contrast, others may adopt a more aggressive approach, preferring to keep less cash at hand in their balance sheets.

Generally, companies maintain a certain cash balance to cover ongoing expenses in case of emergencies, such as unpaid invoices from customers. Cash balance is often compared to total or fixed costs in such situations.

Factors to determine the optimal cash balance

In this context, re:cap analyzes the relationship between cash balance and burn rate, as well as its proportion to total costs. These metrics serve as indicators of what an ideal cash balance might look like.

However, defining an optimal cash balance depends on the individual characteristics of each company. Key questions for further clarification may include:

- How do I finance my total capital requirements?

- What is an appropriate cash balance for companies with a specific cost structure?

- What is my total capital requirement?

- What is my capital requirement at each point in time?

- What is my burn rate?

Interested in your funding scenario?

Get access to re:cap and calculate your funding terms or talk to one of our experts to find out how we can help you with our tailored debt funding.

Calculate your funding termsHow does re:cap help companies with their cash balance?

Scenario 1: A company wants to avoid falling below or maintain a specific cash balance

Let's first examine the initial scenario. A company has set various requirements regarding its cash balance:

- I'd like to have a positive cash balance.

- I want my cash balance to always have a certain amount as a minimum.

These objectives raise the question: How do I finance my business plan under these conditions?

Companies plan their cash flow based on their business plan.

They forecast their future earnings and expenditures to determine their financial needs. This sets the stage for planning their financing tactics, whether it's timing, amounts, or the instruments used.

The dance of cash balance and financing

Now, companies can utilize various sources of capital for financing. For some financing projects, debt may be more suitable, while for others, equity may be preferable.

If a company opts for debt and wants to use an alternative financing instrument as offered by re:cap, re:cap first analyzes its business plan in conjunction with the initial cash balance objectives. From there, a funding plan is developed.

How does this work?

How capital amount and timing impact cash balance

Various capital needs are outlined in the business plan, each occurring at specific points in time. The company requires additional funds at these junctures.

Without them, not only can the goals of the cash balance be jeopardized, but the company as a whole may come under pressure due to the imbalance in the cash balance.

Let's take a look at the cash flow plan of a sample company. In its business plan, it has identified a funding need of €2 million over 12 months.

- July: €500,000

- November: €500,000

- March: €500,000

- July: €500,000

Two funding options: lump sum vs. flexible drawdowns

- It can acquire one large sum at once. However, this almost always leads to higher capital costs. The company doesn't need the total sum immediately but rather selectively over eighteen months.

- It can opt for a flexible financing model, providing capital at the appropriate times. The company utilizes the funds directly, avoiding a constant drain on its account.

While re:cap caters to both options, the latter often proves more cost-effective. With flexible financing, companies access capital as needed, maintaining a healthy cash balance without draining their accounts.

Using re:cap's flexible credit line

With the second option, companies don't receive a large funding all at once. re:cap provides a flexible financing line, allowing the company to access different amounts of capital at different times, depending on their funding plan. This enables companies to acquire capital cost-effectively.

The company's funding profile indicates its financing limit (the maximum amount of capital the company can receive based on its ARR) as well as its utilization of re:cap.

With this approach, the timing and amount of funding are tailored to the business plan and the current company's development. The revolving financing volume decreases or increases according to the company’s needs.

Thus, re:cap combines two aspects: flexibility and long-term stability.

Flexible and long-term financing for an ideal cash balance

Debt funding from re:cap is flexible. Companies can determine every month how much capital they need.

However, the financing plan is not rigid. It is adjustable to new business developments, investment opportunities, or market conditions.

Especially for early-stage companies, it's crucial not to commit to fixed financing but to stay flexible and decide when and how much capital they need.

Adaptable financing that grows with your business

On the other hand, re:cap can be used long-term. Companies can repay it over five years – and choose their grace period flexibly.

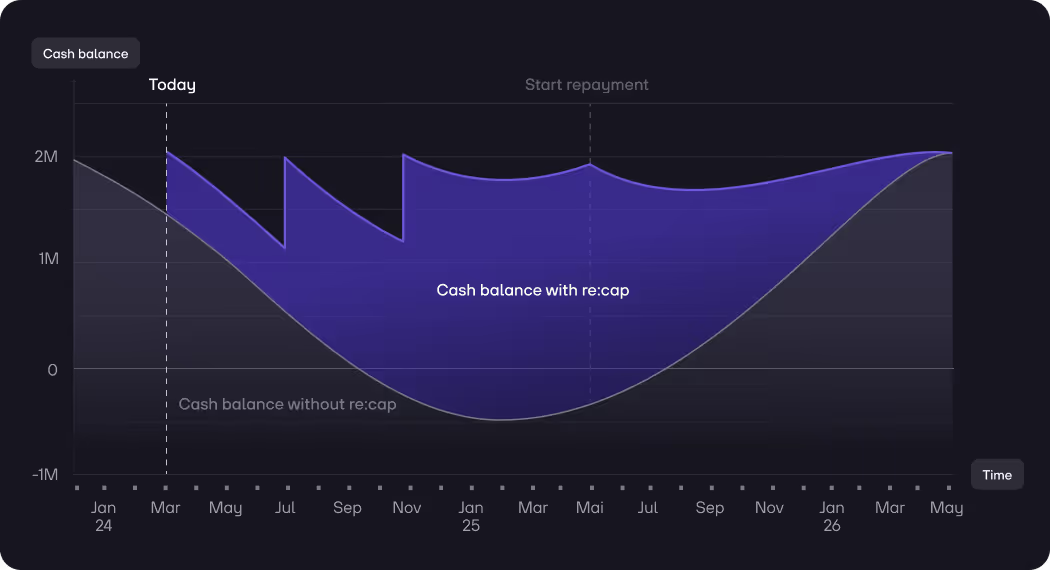

Example: how flexibility protects your cash balance

Let's consider an example with a grace period of 12 months. The company repays its funding over a four-year term. After six months of repayment, an opportunity for growth arises. The company wants to invest.

With other debt instruments, investment and repayment would burden the cash balance. With re:cap, the company can suspend its repayment, invest, and simultaneously maintain its aimed cash balance.

This flexibility enables companies to achieve an ideal cash balance without risking unnecessary capital costs and simultaneously use growth capital to invest.

Tailor cash balance and financing to your needs

Cash balance isn't just about keeping the lights on. It's about covering operational costs, fueling investments, and buffering against uncertainties. Finding the right balance ensures agility and stability, aligning revenues with expenses for a healthy bottom line.

Cash balance is one of the most critical parameters for companies. Planning ahead and being prepared for uncertain times is crucial, as having €0 in the bank is rarely a good idea.

Constantly hovering around this value seldom contributes to positive company development. Instead, companies should be proactive rather than reactive.

Cash balance is an individual figure

However, what constitutes an adequate or ideal cash balance must be defined by each company individually. While having cash at hand is advantageous, having too much can also be detrimental.

Therefore, flexible and long-term financial planning is essential, allowing for adaptation to new situations and corporate goals, while providing the necessary flexibility for companies.

Key questions for an optimal cash balance

Summary: Cash balance

Cash balance refers to the liquid funds a company has on hand to cover operational costs, invest in growth, and protect against uncertainties. It’s a critical financial metric that must be tailored to the company’s specific cost structure, burn rate, and funding needs.

Striking the right balance is essential: too little cash can endanger operations, while too much can lead to unnecessary capital costs. Strategic cash planning means forecasting future needs and aligning them with financing to ensure stability and flexibility over time.

re:cap supports companies in maintaining an optimal cash balance through flexible, tailored debt financing for startups and tech companies. Instead of providing one large lump sum, re:cap enables businesses to draw funds in stages, based on their business plan and actual needs.

This approach helps reduce capital costs, preserve liquidity, and adapt financing to new developments. It ensures that companies stay agile, invest when it counts, and never risk falling below their target cash threshold.

Q&A: Cash balance

What is the cash balance?

The cash balance is the amount of liquid funds a company has available at a given moment, typically cash in the bank or short-term deposits. It’s what you use to pay salaries, rent, suppliers, and other day-to-day expenses. Think of it as your financial safety net and operating fuel.

How do I read the cash balance?

You can find the cash balance on your balance sheet under "current assets." It tells you how much cash or cash-equivalent resources you have available. To understand it in context, compare it to your monthly burn rate (expenses) or total liabilities. A healthy cash balance covers several months of fixed costs without dipping into reserves.

What does the cash balance say about my company?

Your cash balance signals how financially stable and flexible your company is. A strong balance means you're well-prepared for operating needs and unexpected expenses. Too little cash might suggest liquidity risk, while too much idle cash can indicate inefficiency or missed investment opportunities.

How can I improve my cash balance?

You can improve your cash balance by tightening cash flow management, speeding up receivables, delaying non-critical payables, and cutting unnecessary costs. On the financing side, flexible funding solutions like re:cap’s revenue-based financing help align capital access with your actual needs, keeping your cash balance stable without overspending on capital.

Interested in your funding scenario?

Get access to re:cap and calculate your funding terms or talk to one of our experts to find out how we can help you with our tailored debt funding.

Calculate your funding terms.png)